Your Grocery Bill Is About to Soar

Printing cash and handing it out to people for doing nothing is a terrible idea. Prices would go through the roof! You can prepare for this: If you don’t own these two precious metals yet, you need to act fast.My Highest Conviction Trade Ever

If you really like a stock, do you make it 1% of your portfolio? 50%? There are no hard and fast rules, but you can use Jared’s framework for sizing your investments.Now Is Your Chance to Pay Off Your Mortgage in 10 Years

Mortgage rates are the lowest they’ve been in history. Now is the time to refinance and pay off your house fast. You’ll save money, lower your financial stress, and make yourself happier!

What the Coast Guard Taught Me About Fraud

We all start out know nothing about money. But if you don’t learn the basics, you leave yourself vulnerable to hucksters and frauds. That’s what happened to Jared’s Coast Guard buddies...

Gold Isn’t Great for Buying Pizza… But You Still Want to Own Some

Gold is not great for buying pizza, but it does a fantastic job of holding its value. This is one of many reasons you want to own some gold right now.

Don’t Risk Your Money on Garbage Stocks… This Is How You Build Real Wealth

Individual investors have no clue what they’re doing.

They’re pouring into the markets and buying a bunch of garbage. I don’t support any of this... people gambling with money they can’t afford to lose.

So today, I’m going to show you how to start investing like a grownup.

First of all, investing has prerequisites. Before you put one penny in the market, you need an emergency fund with at least $10,000 or enough to cover six months’ worth of living expenses, whichever is greater.

You also need to rein in your debt. Pay off your credit cards and car loans before investing. And take a chunk out of any student loan debt, and your mortgage if you have one.

But don’t put off investing indefinitely. If you wait 30 years to pay off your mortgage and start investing, it’s going to be too late.

Invest as Much as Humanly Possible

Once you’ve established your emergency fund and tackled your debts, you’re ready to invest. And you want to invest as much as you can. I mean it—invest as much as humanly possible.

If you’re in your 20s, you want to invest at least 20% of your take-home pay. I’ll walk you through an example—

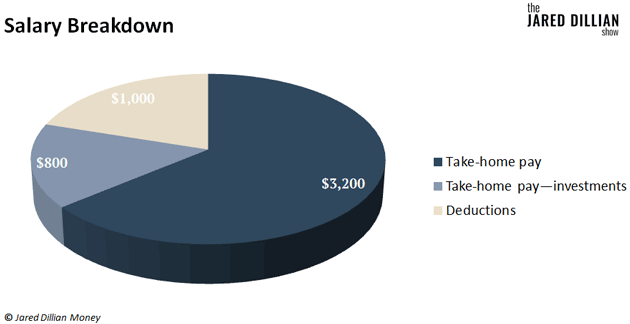

Say your salary is $5,000 per month. Right off the top, about 20% comes out in taxes, Social Security, and Medicare contributions—all the deductions that come out before you see your paycheck.

Whatever is left is your take-home pay. In this example, we’ll say it’s $4,000. So, 20% of that is $800 a month.

This is the minimum you want to invest in your 20s... 20% of your take-home pay.

If you can’t make that happen, look closely at your income and spending. Can you really afford the house or apartment you live in? Are you spending too much on your car or vacations?

For that matter, could you get a new job and make more money?

Only you can answer these questions. But my guess is you could set aside 20% of your take-home pay. You might need to make some changes at first, but over time, this will become a habit.

What if you really can’t set aside 20%?

Do not let perfect be the enemy of good. If you start investing 10% or 15% of your take-home pay when you’re 22, you are light-years ahead of the guy who’s investing nothing, even if he’s earning more money.

The most important thing is to start investing as early as you can. Then work on controlling your expenses so you reach that 20% goal as quickly as possible.

A Late Start Is Better than No Start

What if you’re in your 40s or 50s and just starting to invest?

By now you’re likely earning more, but your expenses have gone up as well. You might have a family, kids, a house—all expensive.

Even so, your goal is to invest half of your take-home pay.

Why so much? First, you’re playing catch-up. Second, your investments will compound over time. That means the profits you earn will start earning profits.

The other reason to invest as much as possible is your investments may fall in value from time to time. What happens if the stock market plummets over 30% again, like it did earlier this year?

You will need time to recover. The key is to keep investing and building wealth. If you do it right, you’ll be free to spend more in the years to come.

The Big Deal with Compound Interest

I can’t overstate the importance of investing as early and as much as possible. Why? It all goes back to a magical little thing called compound interest.

The simplest way to think of compound interest is “interest on interest.” Instead of just earning interest on your initial or principal investment, the interest you earn gets added back into the principal… and you earn interest on it as well.

Compound interest makes a massive difference in your overall returns. Let’s look at an example—

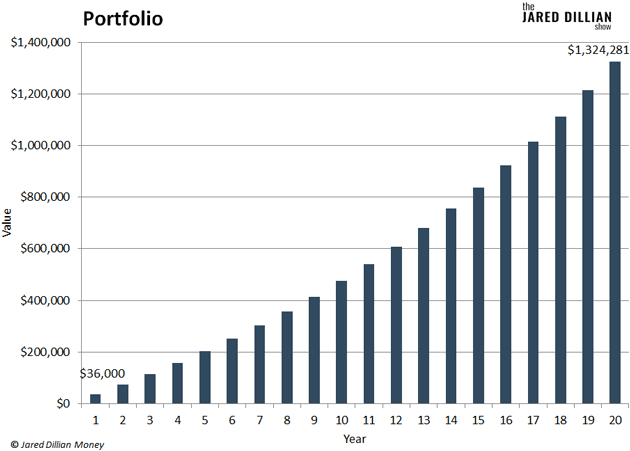

Say you’re 45 years old, and your take-home pay is $6,000 a month. You’re just starting out, so you wrangle in your expenses and invest 50% of your take-home pay. That’s $3,000 a month or $36,000 a year.

Over the next 20 years, your investments return 6% on average. Don’t touch those returns! Leave them in your investment account, and they will start making money for you, too. By the time you’re 65 years old, there’s $1.32 million in your account.

Not bad, especially considering you only started to invest in your 40s.

Where to Invest

Everybody loves stocks. Everybody wants to buy stocks.

But here’s the thing... you should NOT put all of your investments in the stock market.

Instead, you want to hold some stocks, some bonds, some cash, some gold, and some real estate. This is the best way to steadily grow your wealth over time and cut your risk of losing money to the bare minimum.

Of course, there’s a lot more to it than “some of this, some of that.” Which is why I’m so excited to share my new special report with you today. It’s called The Awesome Portfolio, and inside you’ll find the exact 5 investments you want to buy and hold right now.

It pains me to see countless investors buy garbage stocks, risking hard-earned dollars they can’t afford to lose. But you can avoid all that... and start safely investing in your future. Click here to access your copy of The Awesome Portfolio at a steep, limited-time discount.

Jared Dillian

|

‹ First < 35 36 37 38 39 > Last ›